FMCG market in India is showing mixed signals

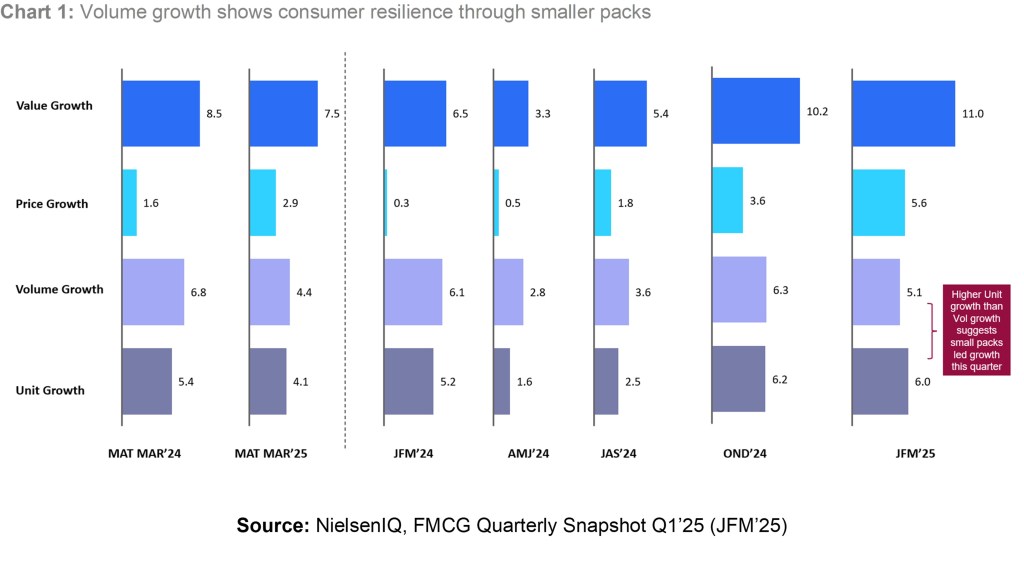

NIQ’s FMCG Quarterly Snapshot for Q1’25 (JFM’25) reveals that the Indian FMCG industry has achieved a 11% growth in value vs Q1’24, reflecting strong resilience. Consumption-driven demand was attributed to a 5.1% rise in volume with a 5.6% increase in prices. A higher unit growth than volume growth indicates preference shift towards smaller packs in consumers.

The FMCG sector is showing mixed signals—while volume growth is slowing across categories, non-food segments are still outpacing food. Inflation is easing overall, but high edible oil prices are keeping staples expensive. Rural markets continue to drive growth, whereas urban metros continue to see a shift toward E-commerce with higher shopper engagement. With a favourable monsoon forecast and revised tax slabs, consumption is likely to pick up in the upcoming quarters. Interestingly, small players are gaining more ground due to a low base and changing market dynamics, though their long-term momentum remains to be seen.”

Roosevelt Dsouza, APAC Head of Customer Success – FMCG, NielsenIQ India

Market Dynamics: Rural demand fuels FMCG growth

In Q1 2025, rural consumer demand grew at a slower pace compared to Q1 2024, yet it remained four times faster than growth in urban areas, where consumption further decelerated. Rural markets continued to outperform urban counterparts s across most regions of India. Traditional trade volumes increased to 6.2% in Q1 2025, from 5.0% in Q1 2024.

Rural Demand Boosts HPC Growth Amid Slowing Food Consumption in Q1 2025

Food consumption growth slowed to 4.9% in Q1 2025 from 6.0% in Q4 2024 (see Chart 3), primarily due to decreased volumes in staple categories like edible oils and Palm Oil, which saw price increases. Home and personal care (HPC) categories experienced a consumption growth of 5.7% in Q1 2025, with higher demand in rural areas.

Over-the-counter categories, such as rubefacients and analgesics, saw a 14.0% growth in value sales in Q1 2025, driven by a 10.4% increase in prices.

E-commerce gaining salience

E-commerce continues to strengthen its presence significantly in 8 metros, impacting the share of offline channels – both Modern Trade (share 22.8%, share change vs. YA: -2.8) & Traditional Trade (share 62.5%, share change vs. YA: -1.5). This growth is largely volume-driven (Metros – E-comm: +39.9% vs. TT: -2.2%, MT: -7.7%), supported by increasing online shopper penetration, more purchase occasions, and increasing basket sizes (more units purchased per shopper).

Steady gains for small manufacturers

Small manufacturers are leading the way in driving consumption, supported by steady volume growth in both Food and HPC categories. In contrast, larger players are experiencing slower volume growth, which has halved compared to Q4 2024. Low base, rural growth, and easing out inflation are helping small players to outpace FMCG growth.

Transform data into actionable strategies

Explore our Thought Leadership Reports—your gateway to winning strategy and stronger outcomes. From high-level macro insights to deep-dive category trends, we’ve got you covered with actionable intelligence to fuel your next move.